Published on:

When the bond amount exceeds what a family can cover with the 10% premium alone, the bail bondsman and the surety insurance company backing the bond will require collateral. For most Florida families, the most significant asset they own is their home. Using real estate as collateral for a bail bond is common practice, but it is a serious financial commitment that creates a recorded lien against the property. Understanding the mechanics of this process, the equity requirements, and the specific risks involved is essential before signing any paperwork.

When Real Estate Collateral is Required

Not every bail bond requires collateral. For bonds under $10,000, many agencies will post the bond based on the 10% premium alone, relying on the indemnitor's contractual liability as sufficient security. Collateral requirements typically kick in for bonds above $25,000, though the exact threshold varies by agency and surety company.

The general guideline is that the surety company requires collateral with a value equal to or greater than the full face value of the bond. On a $100,000 bond, the surety company wants to see $100,000 or more in pledged collateral, in addition to the $10,000 premium.

The Equity Requirement

The bondsman does not evaluate your property's market value in isolation. They evaluate your equity, which is the difference between the property's current market value and all existing liens (mortgage, home equity loans, tax liens, etc.). A home worth $300,000 with a $250,000 mortgage has only $50,000 in equity, which may not be sufficient to collateralize a high-value bond.

Home market value: $350,000

Existing mortgage balance: $200,000

Available equity: $150,000

Bond amount: $100,000

Result: The property qualifies. The $150,000 equity exceeds the $100,000 bond face value.

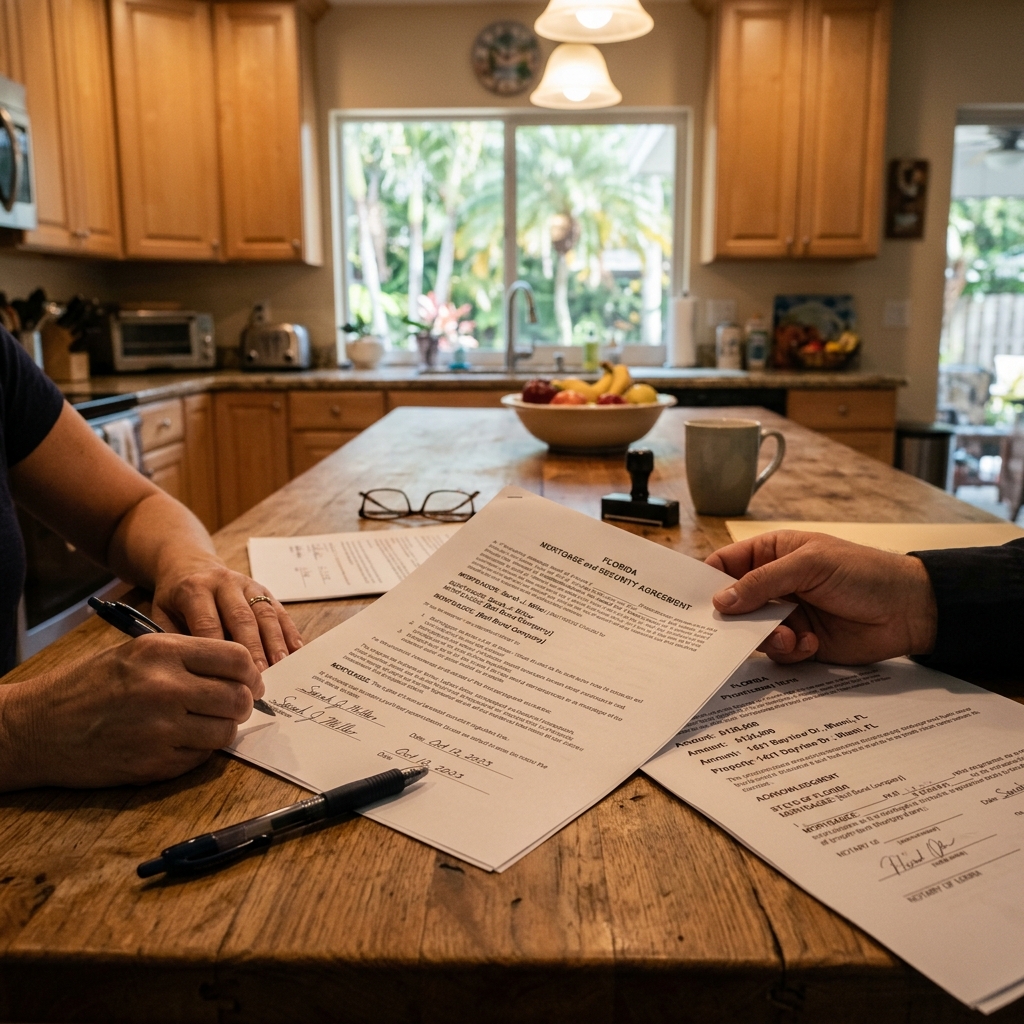

The Lien Recording Process

If the property qualifies, the bondsman prepares a lien document (sometimes called a deed of trust or mortgage for bail bond purposes) that is signed by all property owners and recorded with the county recorder's office in the county where the property is located. This recorded lien is a public record and will appear on any title search conducted on the property.

The lien recording process includes several steps:

- Title search: The bondsman or surety company orders a title search to verify ownership, existing liens, and the property's legal description.

- Property appraisal: The surety company may require a current appraisal or accept the most recent tax assessment value, depending on the bond amount and their internal policies.

- Document preparation: The lien documents are prepared by the bondsman's office or by a title company.

- Signing: All property owners must sign the lien documents. If the property is jointly owned by a married couple and only one spouse is the indemnitor, both spouses must still consent to the lien under Florida's homestead protections.

- Recording: The signed lien is submitted to the county recorder's office and becomes part of the public property records.

Florida Homestead Protections

Florida has some of the strongest homestead protections in the country under Article X, Section 4 of the Florida Constitution. However, homestead protection primarily shields the property from forced sale by unsecured creditors. When a property owner voluntarily signs a bail bond lien, they are consenting to a secured claim against the property. This voluntary lien can be enforced if the bond is forfeited, even against homestead property.

What Triggers Lien Enforcement

The lien sits dormant as long as the defendant complies with all conditions of the bond: appearing at every scheduled court date and adhering to all release conditions. The lien is only enforced if the defendant fails to appear, the bond is forfeited, and the surety company is unable to recover the defendant within the statutory window (typically 60 to 120 days).

If enforcement proceeds, the surety company can initiate foreclosure proceedings on the liened property to recover the forfeited bond amount. This is the worst-case scenario and the reason families must be absolutely certain of the defendant's commitment to appearing in court before pledging their home.

Getting the Lien Released

As detailed in our collateral return guide, the lien is released when the bond is discharged. The bond is discharged when the criminal case concludes by any means: dismissal, acquittal, conviction, or completed sentence. The lien release process takes 2 to 6 weeks after discharge and involves the bondsman filing a lien release with the same county recorder's office where the original lien was recorded.

Frequently Asked Questions

Can I use property in another state?

Some surety companies accept out-of-state real estate as collateral, but many prefer Florida property because the lien recording and potential enforcement are simpler within the same state. The title search and appraisal process for out-of-state property takes longer and may involve additional fees.

What if the property has multiple owners?

All owners must consent to the lien. If the property is owned by three siblings and only one is the indemnitor, the other two must agree to have the lien placed on their ownership interest. Without unanimous consent, the lien cannot be recorded.

Can I refinance my mortgage while the bail bond lien is in place?

Yes, but the bail bond lien will appear on the title search, and the refinancing lender will need to subordinate the bail bond lien or require its release before closing. This can complicate the refinance process and may require coordination between the bondsman, the surety company, and the new lender.